When we talk about oscillators in trading, it is easy to relate to the most known ones, such as Relative Strength Index (RSI), the Stochastic Oscillator, or the Commodity Channel Index (CCI). There is one in particular that I have not tested, called Money Flow (MFI), and I would like to see in this article if it works on the futures markets.

Table of Contents

Money Flow index calculation

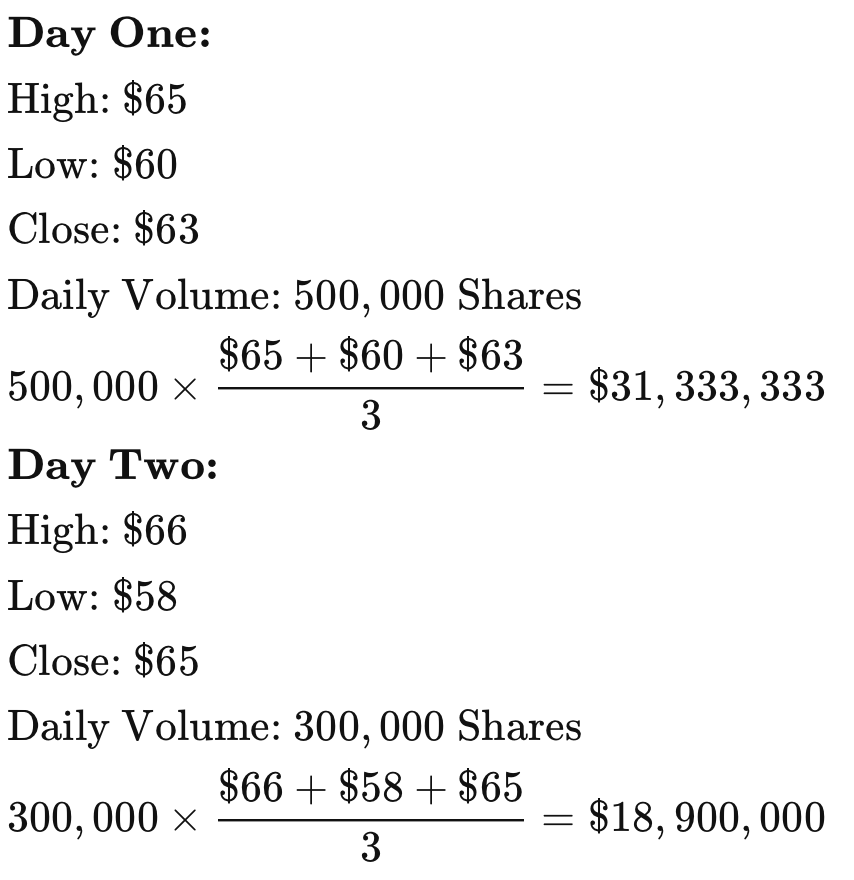

Money flow is calculated by averaging the high, low and closing prices, and multiplying by the daily volume. Comparing that result with the number for the previous day tells traders whether money flow was positive or negative for the current day. Positive money flow indicates that prices are likely to move higher, while negative money flow suggests prices are about to fall.

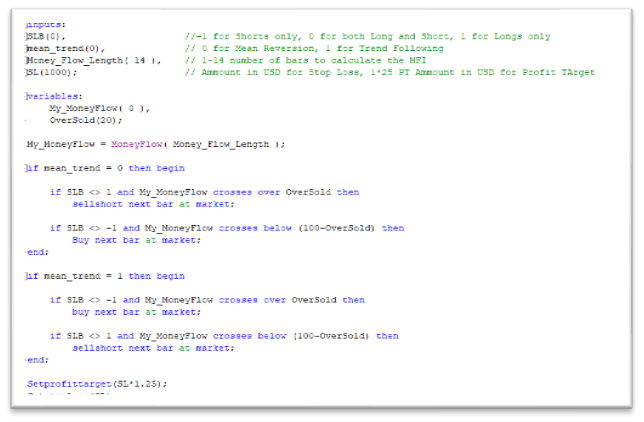

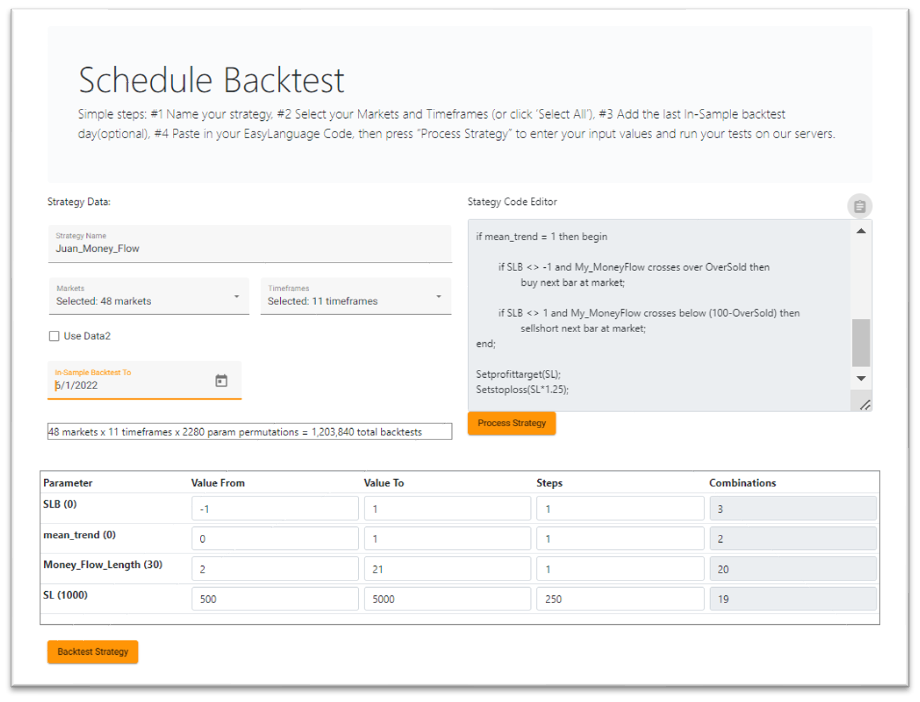

Now let’s proceed to upload the code into Tradesq and select the parameters, Markets, and Timeframe that we want to test:

Note: I like to leave the last six months of unseen data, so tradesq will calculate until 06/01/2022.

Results

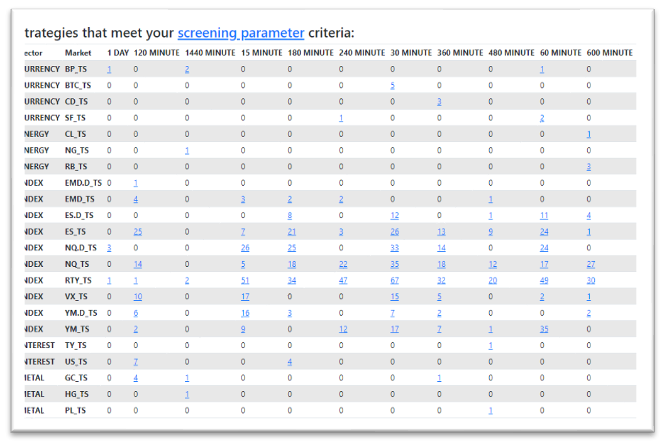

We have a good number of edges on Indexes and very few on the other sectors.

Results filtered by (NP/DD>4, Number of trades above 200)

Let’s have a look at Some results:

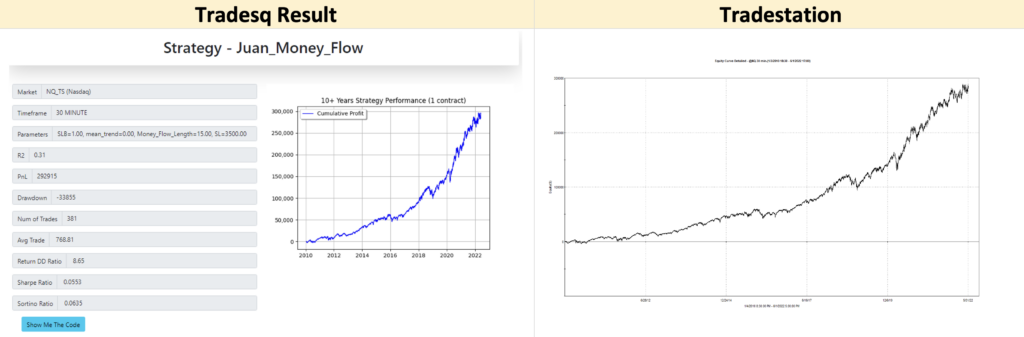

Nasdaq (@NQ) 30min

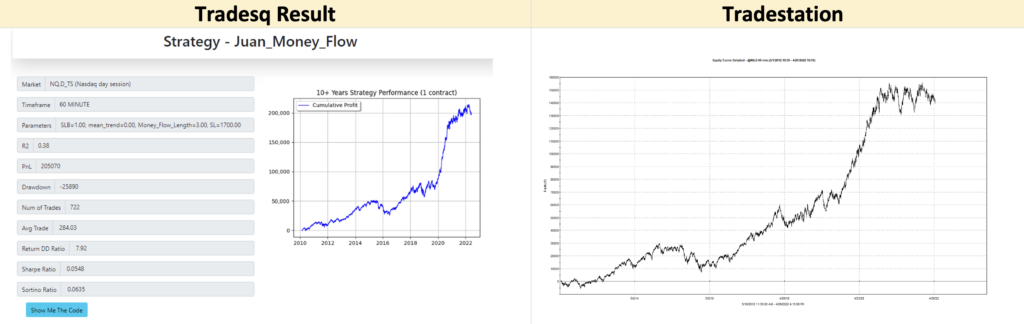

Nasdaq day session only (@NQ.D) 60min

VIX(@VX) 15min

Note: All results include trading costs, Slippage, and Commission.

Conclusion

It’s nice to find that we have other Oscillator options within trading. It could help us diversify and have an edge on the most common ones, as mentioned in the introduction RSI, CCI, ROC, etc. The Money Flow Index Oscillator showed outstanding opportunities in the Index Markets on the long-only positions and short on the VIX. It might need another filter to see if we could have opportunities in the other future sectors.

Leave a Reply

You must be logged in to post a comment.